Systematic management, no exceptions

The same models we use ourselves

Based on your risk profile, we create an investment strategy grounded in research and proven methodology.

Human decisions are often made under pressure with incomplete information. Our models replace that with a consistent, data-driven process built on global market data and quantitative models.

Broad diversification by default

We spread capital across multiple asset classes including equities, fixed income, PE, VC, infrastructure, real estate, and forestry. Broad diversification lowers portfolio risk without sacrificing expected returns. The result is a strategy that holds up over time.

A disciplined, data-driven decision process

Every portfolio model is the result of a structured process that eliminates emotion-driven choices.

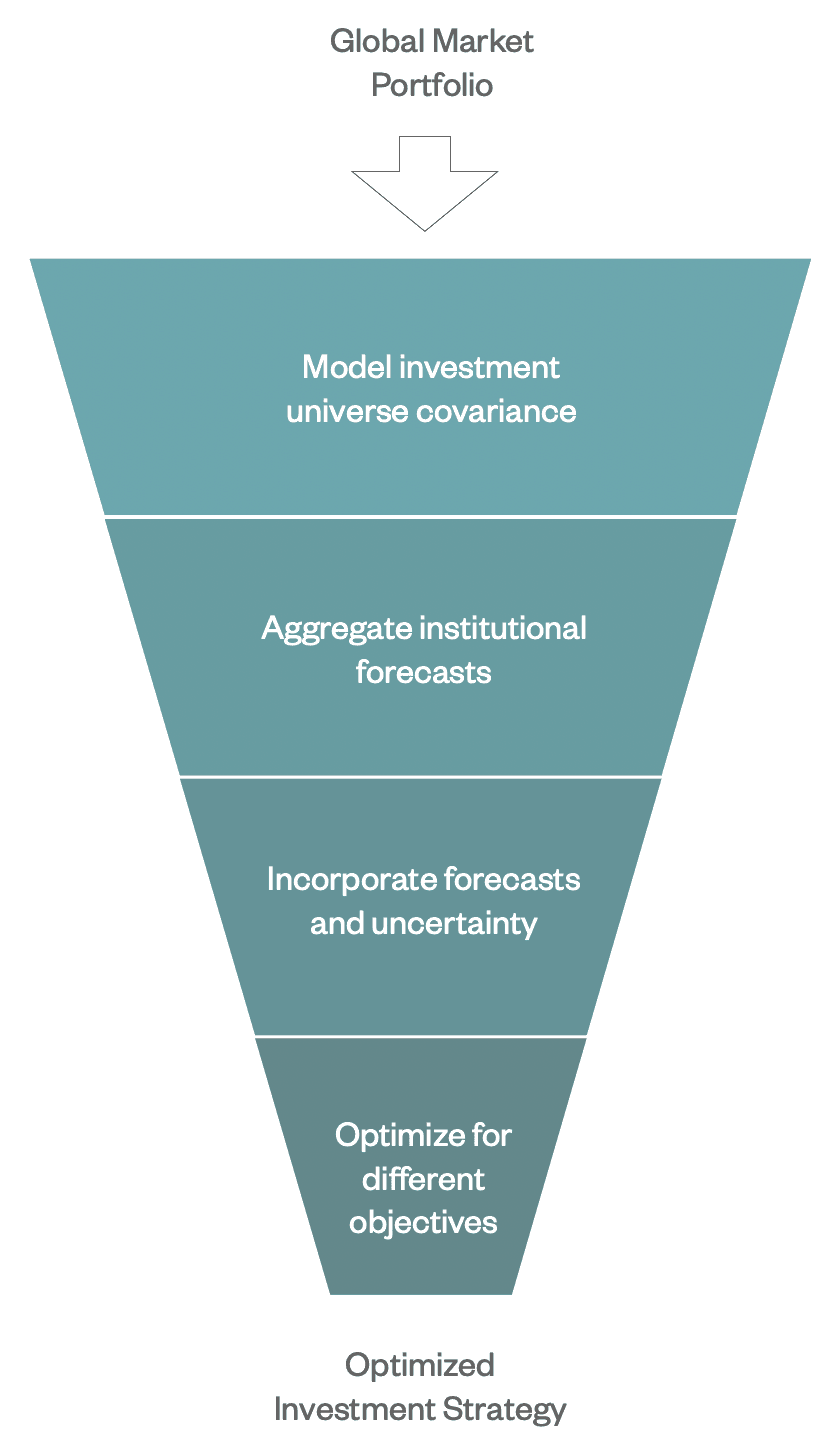

Global market portfolio

We start by analyzing how global capital is actually distributed across asset classes.

Risk modeling

We model the co-movement between assets to understand and control total portfolio risk.

Aggregated forecasts

We integrate return forecasts (CMAs) from leading institutions and factor in inherent market uncertainty.

Optimization

Every asset in the final portfolio is chosen to deliver the best possible net return relative to your goals.

Low costs by default

We build models with a focus on cost-efficient exposure. Costs and market friction are among the biggest value destroyers over time, which is why we analyze them at every step. How the models are constructed and the principles they are built on are disclosed openly. Nothing hidden, nothing unexpected.

How can we help?

We work with companies and investors looking to apply quantitative methods to their investments. Get in touch and we'll figure out what makes sense.