Brent crude surged sharply after the United States and Israel launched strikes against Iran on February 28, reaching a peak of around $110–120 per barrel before pulling back somewhat. Traffic through the Strait of Hormuz, which accounts for roughly 20 percent of the world's oil and LNG flows, has been severely disrupted. Several banks have raised their oil forecasts, but estimates vary widely across different scenarios.

If you are an investor following these events, your gut is probably telling you one of two things. Either sell everything and wait until the storm passes. Or buy oil companies, defense stocks and gold before prices rise further. Both impulses feel rational. Both have historically destroyed wealth.

The average investor vs the market

Every year, DALBAR publishes its Quantitative Analysis of Investor Behavior. The 2025 edition showed that the average equity investor earned 16.54 percent in 2024, while the S&P 500 returned 25.02 percent. That is a gap of 8.48%, the second largest in a decade. Over a twenty-year period, a hypothetical $100,000 invested in the S&P 500 grew to $717,503. The same amount, subjected to the average investor's pattern of buying high, selling low and reacting to headlines, became just $345,614. More than half of the potential return was eroded by behavioral timing decisions.

DALBAR measures what they call the "Guess Right Ratio", meaning how often investors successfully time their entries and exits. In 2024, that figure was 25 percent. Investors guessed the market's direction correctly a quarter of the time. Flipping a coin would have produced better results.

This is not about intelligence. It is about how we are wired. The human brain evolved to respond to threats with fight or flight. When oil prices surge and the news shows drone strikes, the amygdala reacts long before the prefrontal cortex has opened a spreadsheet. The result is predictable: we sell at the worst possible moment and buy back after the recovery is already priced in.

What history tells us about geopolitical shocks

The impulse to sell during a crisis rests on an assumption: that the market will continue to fall. The historical record says otherwise.

LPL Research has examined more than 20 major geopolitical events since World War II. The average decline was 4.7 percent, with a median of just 2.9 percent. Markets typically bottomed within around 19 days and were fully recovered within an average of 42 days.

Research published by Hartford Funds shows a similar picture. One year after an armed conflict began, the S&P 500 was higher in 73 percent of cases, with average returns of 7 percent.

Even during the Cuban Missile Crisis in October 1962, arguably the closest the world has come to nuclear war, the S&P 500 fell about 7 percent during the first four trading days. By November 1, the index had recovered the entire decline, and by year-end it stood in double-digit positive territory.

The obvious counterexample is the 1973 oil embargo, which triggered a decline of 48 percent in the S&P 500 from peak to trough and years of stagflation. That comparison comes up frequently right now. But the structural context has changed in important ways. In the 1970s, the United States was a major oil importer. Today it is the world's largest producer. OPEC controlled a significantly larger share of global supply then. And the coordinated production cuts by several Arab states that defined 1973 have no equivalent in the current conflict, where several Gulf states have interests diametrically opposed to Iran's.

None of this means the current situation cannot get worse. It can. But it does mean that selling your portfolio because of a geopolitical event has, in the vast majority of historical cases, been the wrong decision.

The cost of being on the sidelines at the wrong time

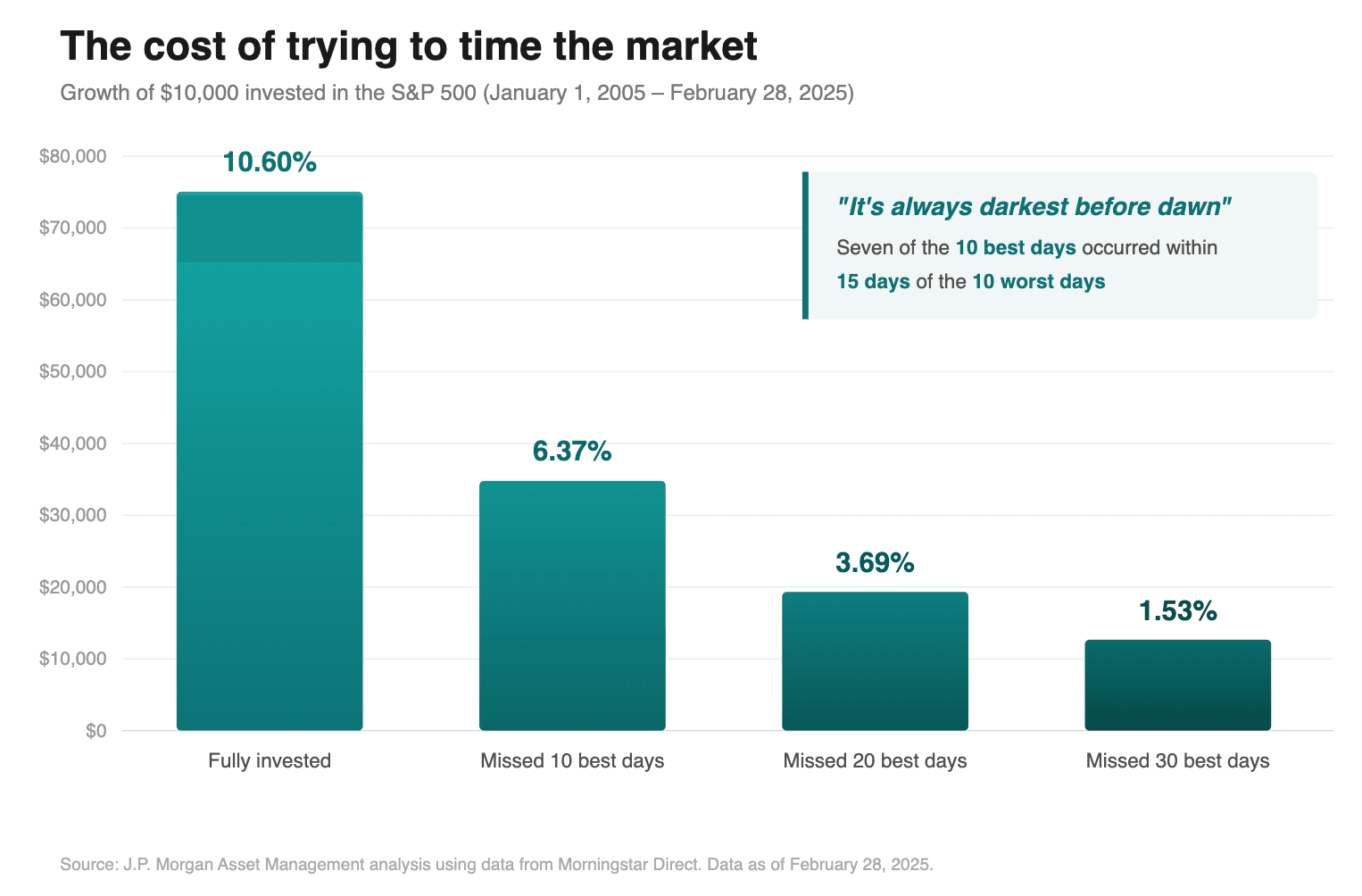

The danger of acting on fear is not just that you sell too cheaply. It is that you miss the recovery.

J.P. Morgan Asset Management has published data showing that if you invested $10,000 in the S&P 500 and stayed fully invested for 20 years, your annual return was 10.60 percent. Miss the 10 best days, and it drops to 6.37 percent. Miss the 20 best days, and you end up at 3.69 percent.

Here is what makes timing nearly impossible: seven of the ten best days during that twenty-year period occurred within two weeks of the worst days. The recovery and the crash sit right next to each other. You cannot capture one without enduring the other.

This is why a systematic, rules-based investment process matters more than conviction, courage or market instinct. A framework does not panic. It does not watch the news. It does not lie awake wondering whether oil will hit $150.

What a quantitative approach does differently

At Markov Capital, we build portfolios using mathematically optimal strategic asset allocation. In plain terms, this means we do not rely on any single analyst's forecast. Instead, we aggregate expected forecasts from a large number of leading global financial institutions, weight them mathematically, and use these consensus estimates as inputs to a quantitative model that balances expected return against risk.

When oil prices surge, our framework does not react to the headline. It incorporates the updated consensus forecasts from dozens of institutions, recalculates expected returns across asset classes, and identifies whether the portfolio needs adjustment, and if so, by how much. Sometimes the answer is a meaningful change. Often a small one. Sometimes the answer is: do nothing, you were already positioned for this.

The value of this approach is not that it predicts the future. No one can do that reliably, and anyone who claims otherwise is probably trying to sell you something. The value is that it removes the most unreliable component from the investment process: human gut feeling.

What investors can do now

If the Iran conflict and the oil price surge are making you worried about your portfolio, that worry is worth examining. Not because the situation is not serious. It is. But because worry is information about your risk tolerance, not information about the market.

Three things are worth considering.

First, review your allocation. If what is happening in the world is keeping you awake at night, you may be carrying more equity risk than is appropriate for your situation. The right allocation is the one you can stick with through a crisis, not the one that looks good in a spreadsheet during calm markets.

Second, make sure you have a liquidity buffer. A cash reserve covering medium-term expenses means you never have to sell investments at a bad time. Forced sales during downturns are one of the biggest destroyers of long-term capital. For investors with assets in multiple currencies, it also matters where that buffer sits. A buffer denominated in euros may be suboptimal if your obligations are in Swedish kronor.

Third, review your process. If your investment decisions are driven by headlines, that is the most expensive variable in your portfolio. A systematic method that aggregates the best available evidence and applies it consistently will not eliminate uncertainty. But it will prevent you from making the mistake that has cost the average investor more than half of their potential returns over the past two decades.

The world is uncertain. It has always been uncertain. The question is not whether you can predict what happens next. The question is whether your process can handle not knowing.

Sources: DALBAR, Quantitative Analysis of Investor Behavior 2025; LPL Research, How Markets Behave During Moments of Uncertainty; Hartford Funds, Military Conflicts May Rattle Markets, But Not for Long; J.P. Morgan Asset Management, Guide to the Markets, Q1 2026; CNBC, Oil Prices: Analysts Raise the Alarm as Crude Soars Over Iran War, March 9, 2026; CNBC, The Economy Has a Strait of Hormuz Deadline for Trump: Two Weeks, March 22, 2026; CSIS, The Iran Conflict Is Sending Oil Prices Soaring.

This text is intended for informational purposes and does not constitute investment advice. Past performance is not a guarantee of future results.